How to Structure Your Bank Accounts for Massive Financial Success

As a freelancer, getting paid is at the top of the priority list. But what do you do with the money once you have it? It's time to structure your finances.

New to freelancing? Start here with my FREE 100+ tip guide.

Price your services, find better clients, and avoid beginner mistakes all in one clear, practical book.

As a freelancer, finding clients and getting paid is always at the top of the priority list. But what do you do with the money once you have it? Where do you put it? How do you manage it on a daily basis?

Most freelancers fail to structure their finances properly due to a lack of time or understanding. The result is a disorganized financial life which can lead to big money problems down the road.

I’m willing to bet that, as a freelancer, you have a single checking account and a single savings account. After all, that’s what most of us are taught to have growing up. While it’s not necessarily bad to run your freelance business that way, I think it’s less than ideal.

After years of having single accounts through Bank of America, M&T, and Simple and using apps like Mint to manage my money, I’ve finally found a system that works well for me. Today, I want to share the details of my system with you in hopes that it will give you the insight and inspiration you need to manage your money more effectively.

Separate Your Bank Accounts

Since you’re starting a business, you’ll need to rethink the way you handle money on payday. The most simple way to do that is by keeping “business money” separate from “personal money”. As a sole-proprietor you won’t qualify for a business checking account, but you can open a second personal checking account.

Some banks may let you open a business checking account as a sole-proprietor, but meeting all the requirements seems like more of a hassle than it’s worth. A second personal checking account can easily be used as a holding bin for your “business money”, though it won’t offer any benefits or legal protection.

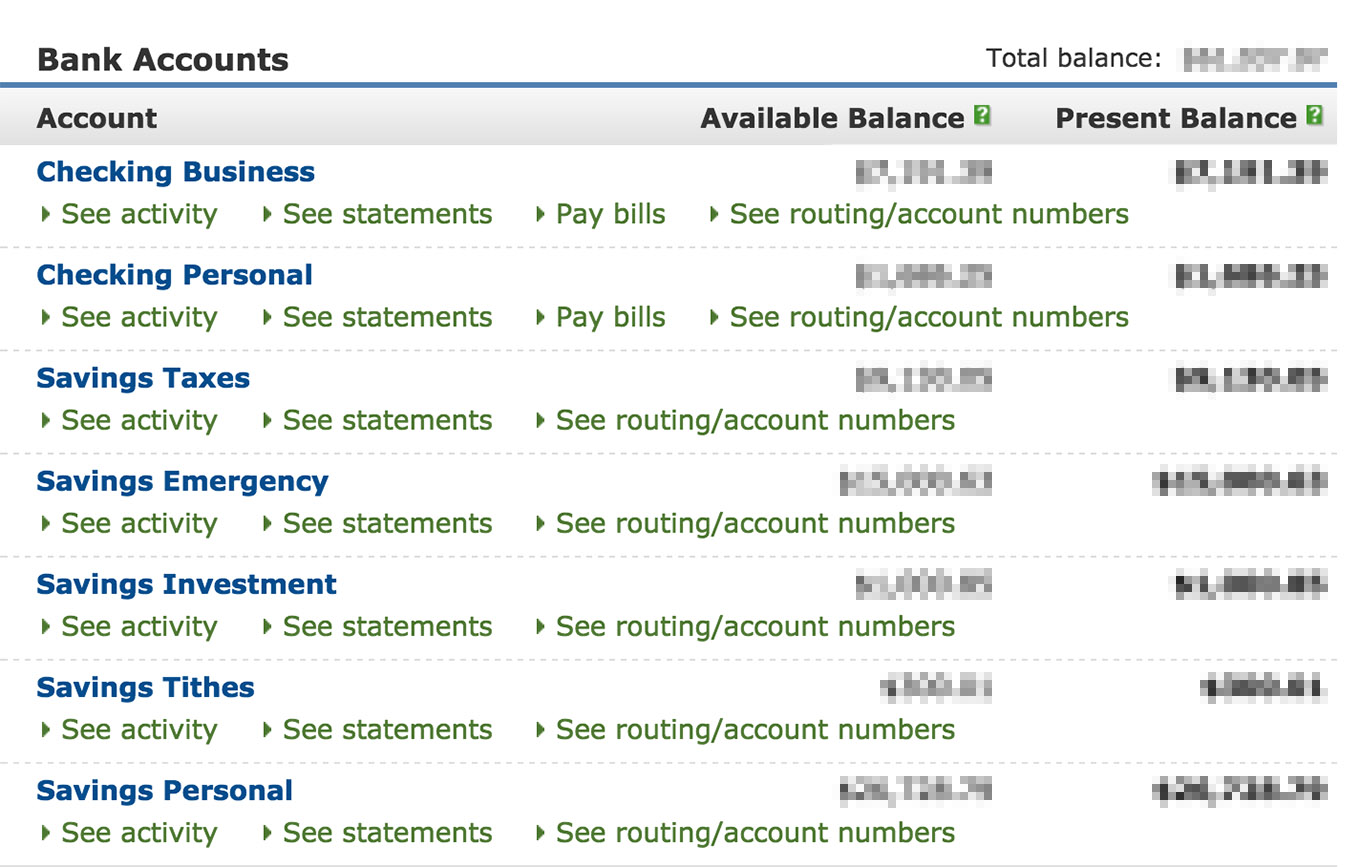

The next thing you’ll want to do is open a few savings accounts. Most people don’t even realize that it’s possible to have more than one, but it is. I bank with Chase and was able to open 5 savings accounts online for free.

You may not need 5, but I recommend you have at least 3 for taxes, emergencies, and personal savings. My other 2 accounts are for tithes and investments.

If your bank allows for it, nickname each account to make money transfers and balance inquiries easier. Here’s what my online dashboard looks like:

Now that you have your accounts setup, you can manage your finances like a pro. Each account will have separate routing and account numbers, billing statements, activity feeds, and balance displays. You should be able to transfer money between them freely and instantly online. If not, consider switching to a bank that allows you to as this functionality is integral to the process.

If this seems like more work, it is. Stick with me. I think you’ll agree it’s worth it.

Why Mint and Bank Simple Don’t Work

Now, you might be thinking of apps and websites (such as Mint and Bank Simple) that claim to do a lot of this “management” and “separation” for you.

I’ve used Mint and Bank Simple for years and I have yet to find an adequate replacement for separating your money at the source by using separate accounts. It’s a manual process, but the more hands-on you are with your money, the more disciplined you’ll be at managing it.

The problem with Mint and Simple is that they’re merely visualizations of your money. When you swipe your card, money still comes out whether you’ve “separated” it or not.

That makes it possible for you to set a budget of $500 a month in one category, but overdraw from a different category if you need to spend more. All the money is in the same place. Having separate accounts is the only way to truly prevent money from moving when you don’t want it to.

✨ Freelance InsightKnowing that the money can come out is the fundamental problem. Separate the money at the source and manually move it when you need it.

Perhaps most importantly, I’ve found that it’s extremely difficult to mentally maintain a running tally on the minimum amount I need to keep in my accounts. For example, if I build up a $15,000 emergency fund in my personal checking account, my account should NEVER drop below $15,000. But since I can see that there’s a bunch of money available, it’s easy to justify spending it.

Likewise, if I have a single savings account that I use for emergencies, taxes, and personal savings, I might be inclined to spend more money than I really have available (regardless of the interface used to display the data). Knowing that the money can come out is the fundamental problem. That’s why I prefer to separate the money at the source and manually move it when I really need it.

Sure, it might be slightly cumbersome to transfer money into your personal account from your business account each month (if you’re like… really lazy or have an annoying bank), but it will also help you increase your savings rapidly. If you have your bills on auto-pay, it’s important that you’re checking in on you’re checking accounts a few times a month anyway.

Pay Uncle Sam

Whenever you get a paycheck, put 100% of it in your business checking account. If it’s pre-tax income (which most of it will be), you need to make sure you pay Uncle Sam first. That’s perhaps the most important step freelancers miss. If you just got a $10,000 check, you only get to keep about $6,000 of it. Ouch.

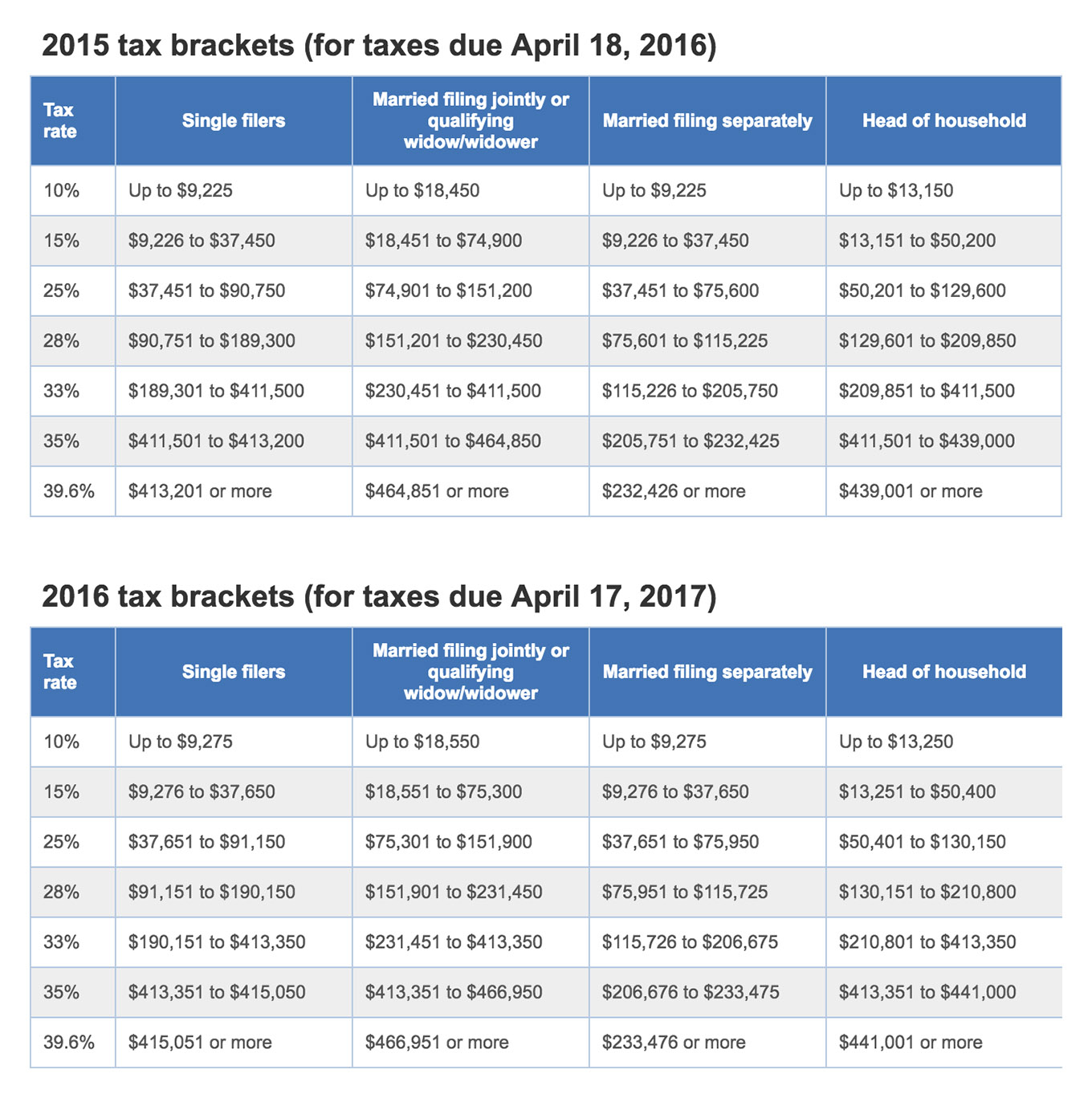

Unlike a normal salary job, you need to pay quarterly taxes on January 15th, April 15th, June 15th, and September 15th. Therefore, it’s best to take the hit immediately before there’s any risk of spending money that isn’t yours.

The tax brackets change a little every year, but here are the federal tax brackets at the time of this writing:

Let’s say you fall into the 28% tax bracket because you’re a rock star. In addition to federal tax, you’ll need to pay state income tax, which (by my crude calculations), is roughly 6% in upstate New York. Finally, you need to pay self-employment tax.

Yes, you get taxed for being self-employed and it’s a whopping 15.3% as of 2015. “How does that work?”, you ask? Well, self-employment tax is similar to the Social Security and Medicare taxes withheld from the pay of most salaried employees.

While it’s likely that you’ll have write-offs and deductions to soften the blow, I recommend putting 40-45% of your income directly into your “Taxes” savings account on payday. That’s definitely not fun, but it’s always better to land right-side-up on your “estimated” tax payments and get a big tax return next Spring. After my first year of freelancing, I received nearly $20,000 in tax returns because I overpaid and had plenty of write-offs. That was a good day.

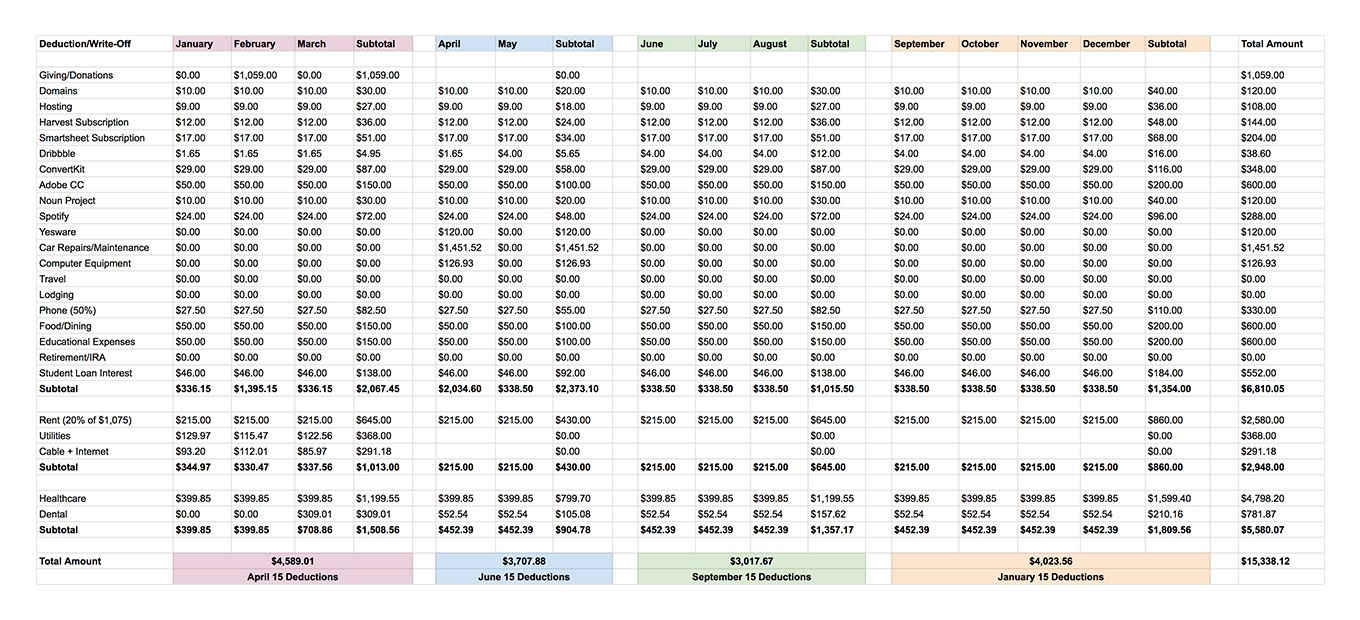

Here’s a sample of the spreadsheet I use to keep track of my write-offs and what quarter they can be deducted in:

You’ll also want to consult a CPA or financial advisor for a breakdown on how much should go to the state and federal government each quarter. Don’t get fooled into thinking you can go to the IRS website and make all your payments.

Wrong. You have to pay state-estimated taxes separately.

I learned the hard way (even after speaking to my accountant), but because I had so much money in savings, the mistake was easily corrected.

When it’s time to make your estimated tax payments, you can withdraw money from your “Taxes” savings account without affecting any other finances. It is possible you’ll get hit with a small fee ($5 or $10) for having a temporary zero balance in a savings account, so be sure to close a new project and replenish it quickly. You can also maintain the minimum required amount in each savings account to avoid potential fees.

Pay Yourself

Once you deposit your paycheck into your “Business” checking account and save money for taxes, it’s time to pay yourself. This is where your “Personal” checking account comes into play.

While there are no tax benefits involved here, this is a simple and effective way to separate your “business” money from your “personal” money.

Money in your business account can be used for business expenses (such as computer equipment) while money in the personal account can be used to pay rent, buy food, and eliminate debt. The “Personal” checking account is what you’ll use on a daily basis.

Related Article: The Net Income Formula: Everything You Need to Know

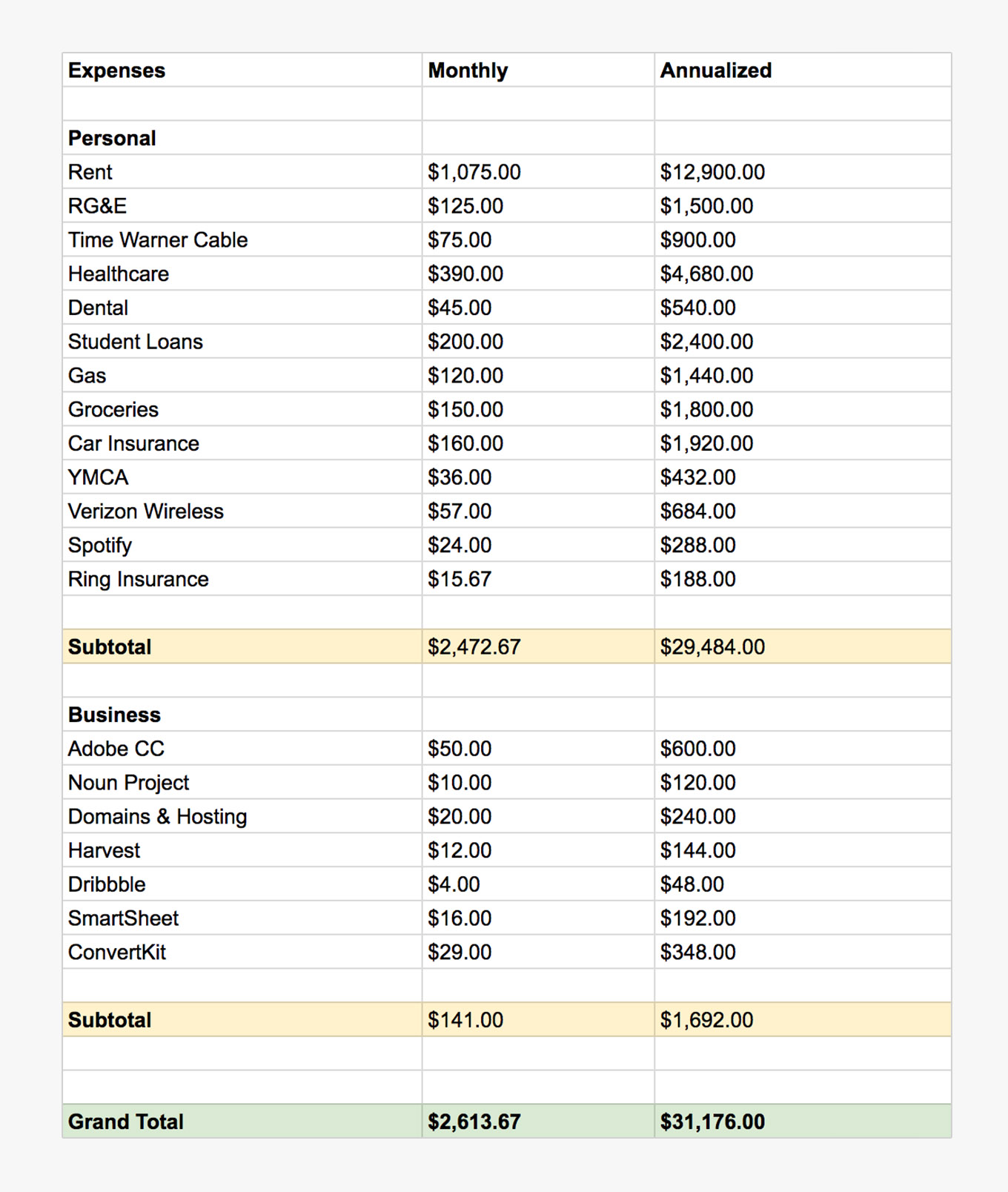

To pay yourself, calculate how much you need each month in order to live the lifestyle you have. Be conservative until you fine-tune this system. Make a realistic budget that includes your bills, expenses, debts, and some spending money on a spreadsheet. Then transfer that amount from your “Business” checking account to your “Personal” checking account once a month. You can update this budget as your lifestyle changes.

Here’s a sample budget I made for your reference:

This budget sheet clearly shows how much you need to earn each month and year to survive. The business expenses can come directly out of your “Business” checking account and the personal expenses can come directly out of your “Personal” savings account. As a bonus, you’ll know that any withdrawals from your “Business” account will count as tax write-offs at the end of the year.

Both checking accounts will come with debit cards which you can use to make separate purchases when shopping online or in stores.

Increase Your Savings

If you have money left over, work on building your “Emergency” savings account first. This is the account you’ll only withdraw from in the event of an emergency such as unexpected medical bills, car repairs, or the loss of a big client. Financial author and motivational speaker Dave Ramsey recommends that you start with a small $1,000 emergency fund until your debts are paid off, then increase it to cover 6 months of unemployment before you invest in personal savings and pay off debt. You can read more about his 7 baby steps to financial freedom here.

Once you’ve built up your emergency fund you can start having fun with your money. Transfer some into your “Personal” savings account for that new car or bigger apartment you want. You can also put some money into an “Investment” savings account which can act as a holding bin while you plan to make wise investments.

Play the Savings Game

With this system in place, saving money becomes fun. My brain treats it like a game. As a visual person, seeing all 7 bank accounts separated at once makes me want to increase the balance each month. Rather than focusing on my next purchase, I’m constantly focused on making the numbers bigger (and making sure they aren’t too small). Then when it comes time to make a big purchase, I have a crystal clear map of where all my money is and which account I should use.

At this point, I’ve given you a lot to keep track of. So, I made this handy flowchart to demonstrate how money should be moved around after hitting your account:

Again, 100% of your income dollars should be funneled through your “Business” checking account first. Then, you can pay Uncle Sam (transfer into your “Taxes” savings account) and transfer the remaining money into your other accounts. Whether you keep some money in your “Business” checking account or transfer it all into savings, every dollar should go somewhere. Be intentional with how you make this system work for you.

Use Google Spreadsheets

I recommend using Google Spreadsheets to keep track of your finances. It’s free, easy, maintainable, and accessible. It’s especially handy if you’re married and sharing the responsibility. There are a lot of nifty apps out there, but nothing can quite replace a blank excel document that you can customize to fit your exact needs.

I have a single master document with multiple sheets in it. That way, I can use Excel functions to automatically update all the sheets when I update my budget sheet. Right now, my “Master Finances” document includes the following 6 sheets:

- Sales Pipeline (project and client tracking)

- Expenses (monthly and annualized budgets)

- Paycheck Divider (where does this money go?)

- Annual Income Log (how much have I actually earned?)

- Tax Deductions (how much can I deduct?)

- Annual Predictions (what happens if I make $X?)

Whenever I get a paycheck, I plug the amount into the Paycheck Divider sheet and it tells me where every penny should go. Next, I log the amount in my Annual Income Log sheet so at the end of the year, I know exactly how much gross and net income I earned.

The Annual Predictions sheet lets me see what life would be like if I earned $X where X is the number I enter. The sheet will then calculate my effective hourly and weekly rate, how many hours and weeks I need to work, how much time off I can have, how much I can spend, how much I should save, etc.

If you’re interested in using these spreadsheets, I’ve made them available for you to download!

Everyone is different. Maybe I’m bad at budgeting. Maybe you are too. Maybe this is way more difficult than what you were expecting. Maybe it’s just what you needed. Regardless, I hope this article inspired you to improve your current system and start managing your money better.

I am not a financial expert. This is just a system that has worked well for me as a sole-proprietor. Thanks for reading!

You Might Also Like These

How to Properly Name Your Freelance Project Invoices

Most freelancers don't spend time thinking about invoice naming conventions, but caring about the seemingly trivial aspects of your business is what will set you apart in the eyes of your clients.

Creating a Financial Foundation for your Freelance Career (A Step by Step Guide)

When it comes to setting up a freelance business, no matter the industry you work in, creating a financial strategy is vital to both your business’ survival and your own personal finance.

5 Common Financial Mistakes Freelancers Should Avoid

As a freelancer, it can seem easy at first to run your business without money management, but in the long-run, a lack of financial awareness or organization can spell ruin for your business.